WORLDWIDEANALYSIS

Due to the expanding construction and automotive industries, the demand for air compressors in the Association of Southeast Asian Nations (ASEAN) member countries is increasing. As a result, the ASEAN air compressor market is projected to witness an increase in its revenue to more than $1,130.0 million in 2024 from $902.9 million in 2018, at a 3.6% CAGR during 2019–2024 (forecast period). Moreover, with the increasing environmental concerns, the requirement for energy-efficient compressors is surging. Air compressors increase the pressure of a gas by decreasing its volume.

The ASEAN air compressor market is bifurcated into dynamic and positive displacement, on the basis of type. Of these, the positive displacement bifurcation held the larger share during 2014–2018 (historical period) due to the increasing demand for these variants in the automotive, industrial manufacturing, power, food & beverage, and construction sectors. The positive displacement bifurcation is further categorized into rotary and reciprocating, of which rotary is the larger and faster-growing kind. Read More: ASEAN Air Compressor Market Analysis and Demand Forecast Report Food & beverage, industrial manufacturing, textile, power, oil & gas, automotive, chemical and cement, construction, heating, ventilation, air conditioning, and refrigeration (HVAC-R), and others are the classifications under the application segment of the market. In 2018, the market was dominated by the industrial manufacturing classification, owing to the rapid growth of this sector in India and China. The Make in India and Made in China 2025 initiatives are driving industrial manufacturing activities in these countries. Moreover, with the Industrial 4.0 revolution, the demand for energy-efficient air compressors in factories is rising. A key trend in the ASEAN air compressor market is the shift from steam and gas turbines as the prime mover to variable-frequency drives (VFD). Electric motors integrated with the VFD technology are replacing turbines as they reduce the downtime of compressors, since they have a lower maintenance requirement. Additionally, the VFD technology offers stronger process control and precise speed and reduces the noise, electricity bills, and capital investments. For instance, compared to the 36% efficiency of a gas-turbine air compressor, one equipped with the VFD technology offers 95% efficiency.

0 Comments

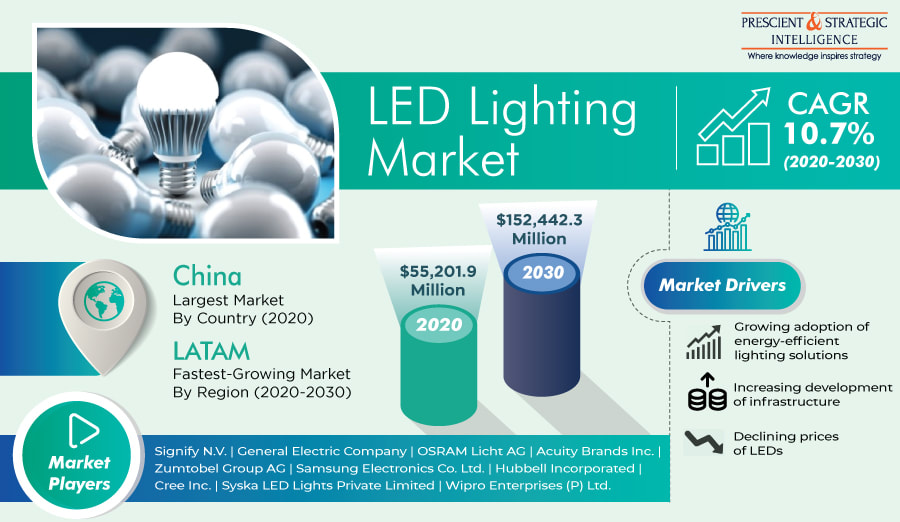

A number of factors such as the growing focus on modernization of infrastructure, declining prices of light-emitting diodes (LEDs), and increasing adoption of energy-efficient lighting solutions are expected to boost the LED lighting market growth at a CAGR of 10.7% during the forecast period (2020–2030). According to P&S Intelligence, the market size is expected to reach $152,442.3 million by 2030 from $55,201.9 million in 2020. Moreover, the market is witnessing a trend of surging adoption of smart LED lighting solutions.

The primary factor improving the LED lighting market growth prospects is the rapid development of infrastructure. As governments of various nations are focusing on the transformation of infrastructure, the need for LED lighting solutions has considerably amplified in recent years. Furthermore, the governments are investing heavily in smart city projects. For example, the Indian government has declared its plans to modernize 100 cities across the nation into smart cities by 2030 and approved about $15 billion for this project, which will drive the demand for LED lights. Likewise, Barcelona, Spain, has installed more than 3,000 LED-based smart streetlights. The product type segment of the LED lighting market is categorized into luminaire and lamp. Of these, the luminaire category accounted for a larger market share in 2020, and it is expected to keep dominating the industry during the forecast period as well, with a higher CAGR. This can be ascribed to the high demand for LED luminaires from new construction projects in the construction industry, along with the growing focus of governments on the implementation of LED solutions, in several countries such as India, China, and the U.A.E. Moreover, based on installation type, the LED lighting market is bifurcated into new and retrofit. Between the two, the retrofit category is projected to witness faster growth during the forecast period. This can be attributed to the surging replacement of sodium-vapor and incandescent lamps with LEDs in various nations, including the U.S., China, India, the U.A.E., Japan, and South Korea. Basically, with the phasing out of sodium-vapor and incandescent lamps in these economies, the need for LED lamps for retrofitting is rising, which, in turn, is boosting the market growth in this category.  The global transparent display market value stood at $524.7 million in 2018, and it is expected to surge to $4,933.6 million by 2024. According to the estimates of the market research company, P&S Intelligence, the market will demonstrate a CAGR of 46.2% from 2019 to 2024 (forecast period). The soaring requirement for transparent displays in the advertising sector and the burgeoning need for smart glass are the major factors fueling the expansion of the market across the world.

The transparent display market is witnessing a massive rise in the requirement for transparent displays for various outdoor advertisement applications, as these displays improve the aesthetic appeal of advertisements. Businesses are rapidly adopting transparent displays for promoting their products via digital signage. The increasing transparent digital signage popularity can be credited to the booming out-of-home (OOH) advertisement industry, which is being driven by the emergence of advanced technology-based retail outlets. In addition, the overall expenditure in the advertisement industry is surging sharply, because of the growing competition among the players operating in the retail industry. This is subsequently pushing up the requirement for transparent displays, that display information regarding services, offers, discounts, and products in a highly aesthetic way. Besides, the rapid technological advancements being made in the healthcare sector are also creating lucrative growth opportunities for the players operating in the transparent display market. This is because these displays are being increasingly required in applications, such as patient checkup and surgery. Additionally, these displays are also being adopted for assisting surgeons during critical procedures, as they display the vital signs of patients, such as blood pressure, oxygen levels, and heartbeats. Depending on application, the transparent display market is divided into digital signage, smart appliance, head mounted display (HMD), and heads up display (HUD) categories. Out of these, the digital signage category contributed the highest revenue to the market in the past.  Compared to 73.407% in 1990, 90.084% of the people of earth had access to electricity in 2019, says the World Bank. This has been a result of the initiatives taken by governments to increase the rate of electrification. Now, while electricity has allowed for innovations in technology, it has itself undergone advancements in the way it is produced, transmitted, stored, and controlled. With the arrival of solid-state electronics, the mechanical switches and relays in power transmission and control systems have been replaced by semiconductor devices, such as thyristors, insulated-gate bipolar transistors (IGBTs), and metal–oxide–semiconductor field-effect transistor (MOSFETs).

As per P&S Intelligence, the growing use of such devices will take the power electronics market size to $20.0 billion by 2022 from $12.9 billion in 2015, at a CAGR of 6.2% between 2016 and 2022. This is because all the solid-state devices that are used for controlling, converting, and transmitting electricity come under the umbrella term ‘power electronics’. Going by this definition, the common household inverter is a power electronic device, since it changes direct current (DC) supply to alternating current (AC) supply without the use of any mechanical (moving) part. Get More Insights: Power Electronics Market Segmentation Analysis Report Another such device is the rectifier, which works opposite to an inverter, changing the AC supply to DC supply. Similarly, the DC–DC and AC–DC converters used in electric vehicle charging systems are examples of power electronics. Thus, even a mobile phone or laptop charger is an example as it takes the AC supply from the socket, changes it to DC, and tones down the voltage to what the electronic device has been rated for. Moreover, every other modern electronic appliance, including LED, LCD, plasma, and OLED TVs, LED lights, washing machines, air conditioners, and refrigerators, have some kind of power electronics. Apart from the consumer electronics sector, the growing automotive sector is an important power electronics market driver. In conventional vehicles, power electronics applications include the interfaces between the engine–alternator and the battery and between the battery and the lights, horns, wipers, starter motors, and infotainment and advanced driver assistance (ADAS) systems. Electric vehicles use power electronics in even higher capacities, as they control the electricity coming from the charging station into the battery and that leaving the battery for the primary traction motor. With the sharp rise in terrorism and security concerns, the demand for physical security solutions is growing rapidly in the Asia-Pacific (APAC) region. Moreover, the increasing security concerns are making various regional countries such as China, India, Vietnam, Indonesia, and Singapore deploy physical security devices and equipment, especially video surveillance systems. There were over 300 terrorist attacks in APAC between 2012 and 2018, with Afghanistan and Pakistan reporting the highest number of terrorist attacks in the region during that period.

Besides the increasing threat of terrorist attacks, the rising prevalence of crimes is also propelling the demand for physical security systems in the APAC region. For example, in China, there were 39,230 robberies, 3,459,742 thefts, and 7,990 homicide cases reported in 2017. Similarly, Malaysia witnessed 379 homicide cases, 42,160 vehicle thefts, 16,200 house break-ins and thefts, and 14,128 robberies in 2017. On the other hand, in Australia, there were 679 homicides, 41,669 thefts, and 3,796 robberies reported in 2018. Read More: Asia-Pacific Physical Security Market Analysis and Demand Forecast Report Apart from the aforementioned factors, the rapid launch of several smart city development projects is also propelling the sales of physical security systems in APAC. In APAC, there are various infrastructural development projects in the pipeline currently. For example, nearly 500 smart city pilot projects are currently in the pipeline in China. Moreover, the country launched the national smart city development plan in 2012 for building smart cities equipped with well-developed infrastructure and transportation systems. Due to the above-mentioned factors, the sales of physical security systems are surging sharply in the Asia-Pacific (APAC) region. This is, in turn, driving the advancement of the APAC physical security market. As a result, the valuation of the market is predicted to grow from $26.3 billion in 2018 to $57.9 billion by 2024. Furthermore, the market is predicted to advance at a CAGR of 14.3% between 2019 and 2024.  Factors such as the increasing concerns about food nutrition, security, and sustainability and mounting investments in plant-based protein sources will drive the meat substitutes market growth during the forecast period (2021–2023). According to P&S Intelligence, the market generated ~$2 billion in revenue in 2020. At present, the surging consumer preference for vegan diets has become a prominent market trend, owing to the growing public awareness of healthy eating habits, hygienic food, and weight management.

One of the key growth drivers of the market is the mounting concerns being raised over food security, nutrition, and sustainability. Food security refers to the state of having reliable access to a substantial quantity of nutritious and affordable food. As per the Climate Change and Land report of the United Nations (UN), food security may be compromised unless there is a transition away from red meat and animal protein sources, such as dairy products, eggs, and pigs to plant-based foods, such as legumes, fruits, and vegetables, which emit lower amounts of greenhouse gases (GHGs) than red meat over their lifetime. Read Full Report: Meat Substitutes Market Revenue Estimation and Growth Forecast Report In recent years, companies operating in the meat substitutes market have been introducing new products according to regional preferences. For instance, in June 2019, DuPont de Nemours Inc. launched a new egg white replacement system for plant-based meat alternatives. Similarly, in July 2020, the company introduced a new range of products under the Danisco Planit brand, which includes plant proteins, enzymes, cultures, hydrocolloids, fibers, probiotics, natural extracts, antioxidants, and emulsifiers. The company focused on nutrition, taste, sustainability, and texture when developing this portfolio. The source segment of the meat substitutes market is classified into pea protein, soy protein, and wheat protein. Under this segment, the soy protein category is expected to generate the highest revenue throughout the forecast period, as soy-based products are rich sources of protein and they resemble the color and texture of meat products. Such products can be used in different recipes and can absorb rich flavors from other food products in a better manner. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

September 2022

Categories |

RSS Feed

RSS Feed