WORLDWIDEANALYSIS

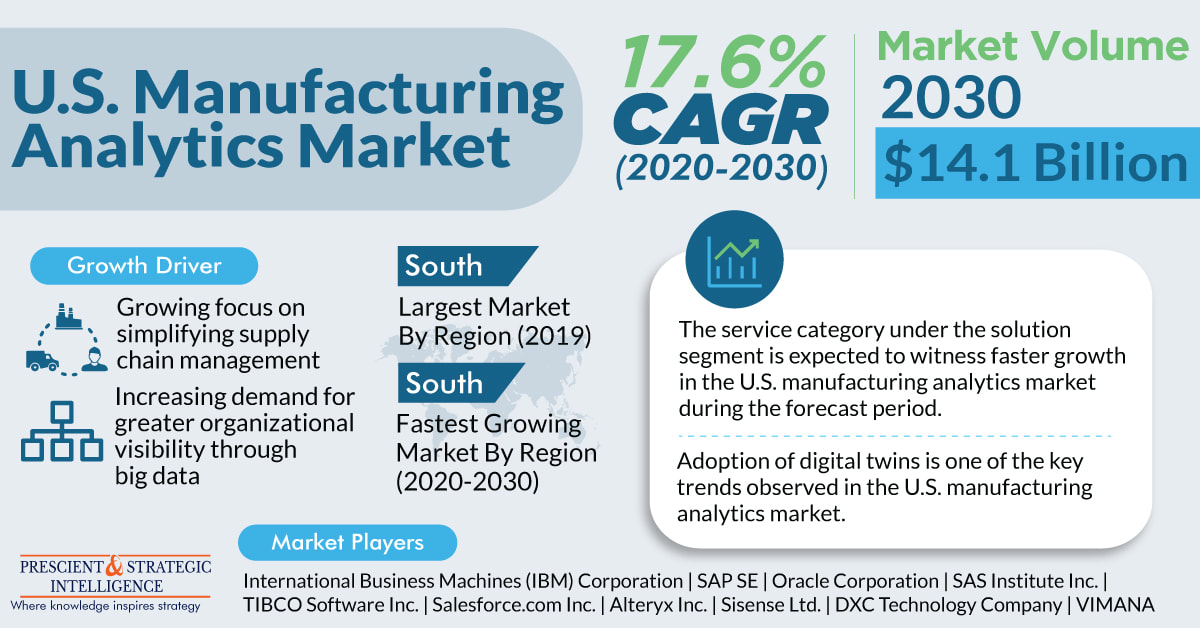

U.S. Manufacturing Analytics Market Predicted to Witness Sharp Revenue Jump During 2020—20309/19/2022  The U.S. manufacturing analytics market attained a valuation of $2.5 billion in 2019 and is predicted to generate a revenue of $14.1 billion by 2030. Furthermore, the market is predicted to progress at a CAGR of 17.6% between 2020 and 2030. The growing requirement for greater organizational and operational visibility via big data and the increasing focus of companies on improving logistics and supply chain management are the key growth drivers of the market.

Big data has revolutionized manufacturing operations around the world, with real-time insights and data collection for analysis becoming rapidly popular among the manufacturers based in the U.S. They can dice and slice the collected data in a way that allows them to gain a holistic understanding of the business activities. In addition to this, big data allows them to optimize operations, address issues and threats before their occurrence, and improve manufacturing. Browse detailed report - U.S. Manufacturing Analytics Market Analysis and Demand Forecast Report Another important factor propelling the growth of the U.S. manufacturing analytics market is the growing focus of organizations on improving the supply chain management process. This is becoming really important in the U.S. manufacturing ecosystem, because of the increasing public awareness about supply chain management, rapid improvements in customer satisfaction levels, increasing control and visibility over inventory, and reducing operational costs. Supply chain management solutions help companies address production needs in various areas such as logistics and manufacturing optimization. Additionally, analytics tools are powering various autonomous and intelligent systems that can be used for streamlining the operations in any stage of the entire supply chain. Depending on deployment, the U.S. manufacturing analytics market is divided into on-premises and cloud. Of these, the on-premises category recorded higher growth in the market in the past. This was because of the higher adoption of this deployment method than the cloud-deployment one, due to its ability to provide greater security of data. Based on industry, the U.S. manufacturing analytics market is categorized into electronics, consumer products, pharmaceutical, automotive & aerospace, food & beverages (F&B), chemical, and oil & gas. Out of these, the electronics industry registered the highest growth in the market in the past. This was because the U.S. is one of the biggest electronics markets in the world and is currently observing a strong competition between the various market players. The U.S. manufacturing analytics market will exhibit rapid advancement in the South region in the future, as per the estimates of P&S Intelligence, a market research company based in India. This would be a result of the existence of numerous manufacturing firms in the region. The abundant availability of manufacturing land and highly-skilled workers for supporting manufacturing operations and the presence of pro-business laws and improved infrastructure are the main factors driving the progress of the market in this region. Hence, it can be said without any hesitation that the market would demonstrate huge expansion across the world in the coming years, mainly because of the rising adoption of big data by manufacturing companies and the increasing demand for better supply chain management from companies around the world.

0 Comments

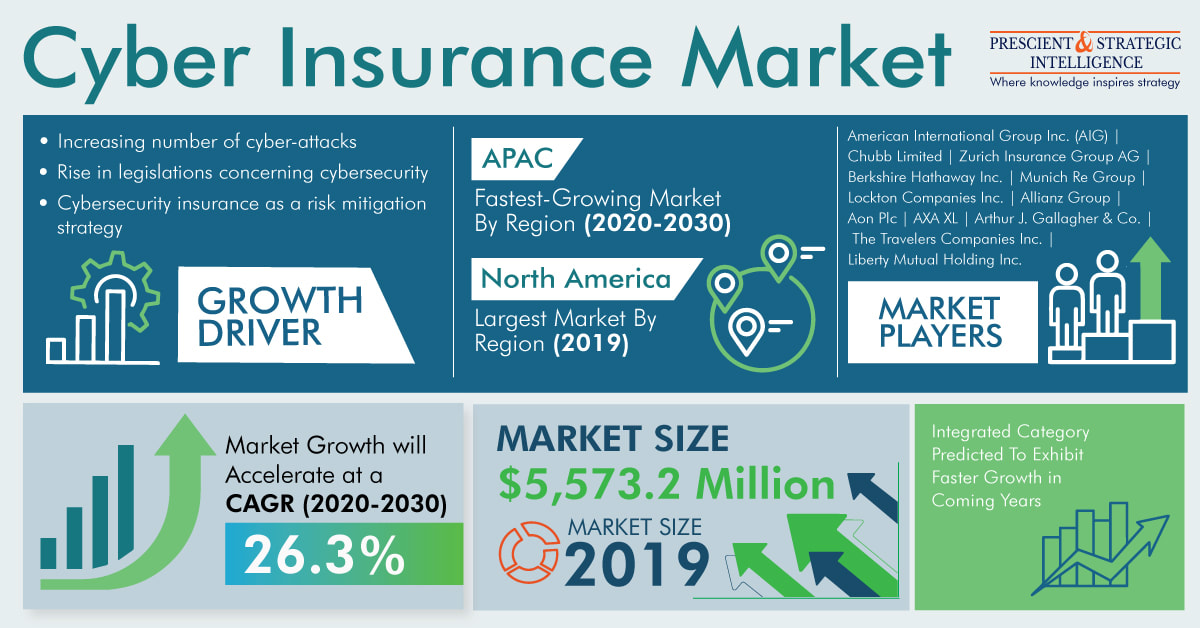

With the growing incidence of cyberattacks and data breaches, the demand for cyber insurance solutions is rising rapidly across the globe. As per several reports, due to data breaches during January 2019– April 2020, around 8 billion records including credit card number, phone numbers, home addresses, and other sensitive and confidential information were exposed. The increasing penetration of the internet and the rapid digitization of enterprise operations are the main factors fueling the incidence of these attacks.

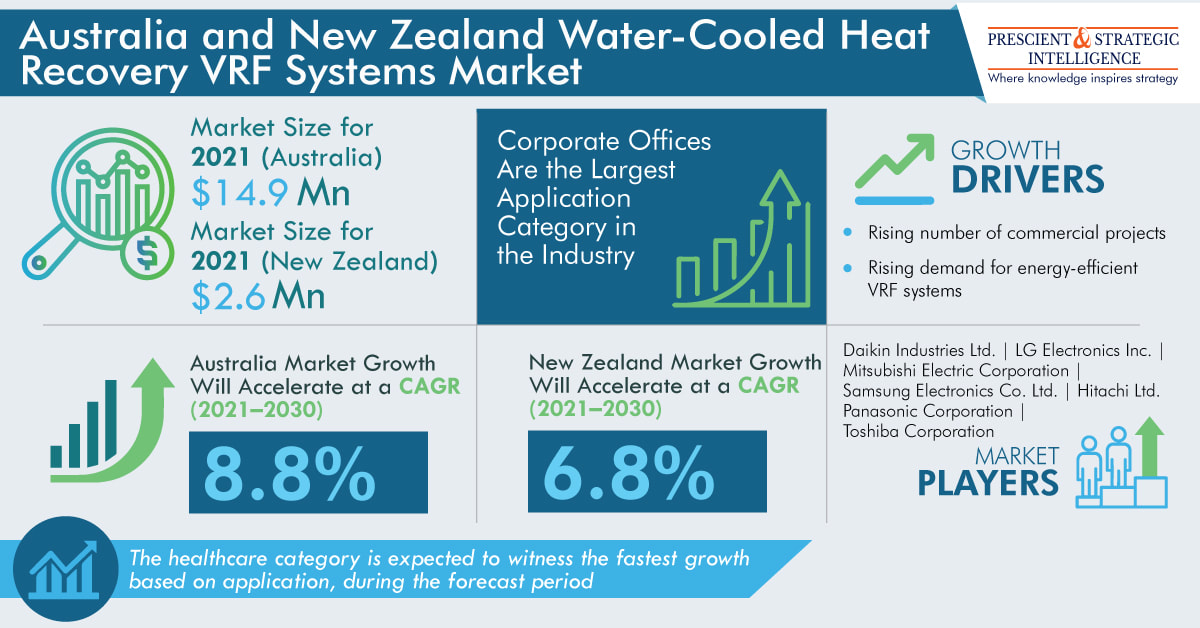

Thus, in order to mitigate the prevalence of these attacks, many governments are implementing policies that make the incorporation of cybersecurity measures and solutions mandatory. As these regulations become more and more stringent and authorities start handing out heavy fines for data breaches, the adoption of cybersecurity solutions including cyber insurance will surge sharply. Additionally, many companies are increasingly adopting cyber insurance solutions as a risk mitigation strategy, thereby driving the expansion of the global cyber insurance market. Browse detailed report - Cyber Insurance Market Analysis and Demand Forecast Report Due to the above-mentioned factors, the value of the market is expected to rise from $5,573.2 million in 2019 to $70,671.9 million by 2030. The market is also predicted to exhibit a CAGR of 26.3% from 2020 to 2030. Depending on type, the market is categorized into integrated and standalone. Between these, the standalone category is predicted to dominate the market in the forthcoming years, on account of its soaring popularity around the world. This is because standalone cyber insurance solutions allow companies to immediately compensate the first and third parties for the losses incurred due to a data breach. These policies reimburse the costs that an insured will incur when responding to a data breach or a cyberattack. This may include information technology (IT) forensic costs, data restoration costs, credit-monitoring costs, public-relation expenses, and cyber extortion costs (such as ransom payments to hackers). When enterprise is taken into consideration, the cyber insurance market is bifurcated into small and medium enterprises (SMEs) and large enterprises. Between these, the large enterprises category is predicted to dominate the market in the upcoming years. This is because of the growing adoption of cyber insurance solutions by large businesses for minimizing the risks associated with various cyberattacks. Moreover, cyber-attackers usually prefer large enterprises to hack, as these companies store large volumes of confidential data. Geographically, the cyber insurance market will demonstrate the fastest growth in Asia-Pacific (APAC) in the upcoming years, as per the estimates of P&S Intelligence, a market research company based in India. This is attributed to the increasing cybersecurity challenges such as cloud security vulnerabilities and attacks on blockchain systems, in the regional countries such as China and India. Additionally, these countries are rapidly implementing policies for improving cybersecurity, which is subsequently fueling the market expansion in the region. Thus, the demand for cyber insurance solutions will rise tremendously in the coming years, primarily because of the growing incidence of cyberattacks and data breaches and the increasing implementation of policies that mandate the incorporation of cybersecurity technologies by the governments of several countries.  The major drivers in Australia and New Zealand water-cooled heat recovery VRF systems market are heat pumps in commercial applications, coupled with a dire need for effective VRF systems. In 2021, product sales in Australia valued at $14,881.0 thousand and at $2,590.8 thousand. Additionally, revenue growth in Australia will be an 8.8% CAGR, and in New Zealand, at 6.8% CAGR in the coming years respectively. At these rates, market players could make a combined $31,739.6 thousand and $4,677.2 thousand by 2030 in Australia and New Zealand, respectively.

The surging population levels will spur the Australia and New Zealand water-cooled heat recovery VRF systems market growth. Thus, this will pave the way for the real estate industry's expansion. Moreover, this will go hand in hand with the increasing number of construction activities in these two countries. Furthermore, there was a 6.2% and 0.4% escalation in the count of dwellings approved in New Zealand and Australia, respectively, during 2017–2021. Also, these magnificent figures show the enormous growth in the construction and real estate sectors of these two countries. Browse detailed report - Australia and New Zealand Water-Cooled Heat Recovery VRF Systems Market Analysis and Demand Forecast Report The extensive government support will create lucrative opportunities for the Australia and New Zealand water-cooled heat recovery VRF systems market players assisting them to adapt to the existing dynamics of the circular economy. This is accompanied by a rising inclination toward green buildings. Furthermore, this will result in skyrocketing demand for VRF systems in these countries because it is an all-in-one device: providing complete air conditioning, ventilation, and heating solutions for the building. New Zealand aims for completely carbon-free newly constructed buildings by 2030. The outbreak of COVID-19 had ruptured the entire circular economy, and the Australia and New Zealand water-cooled heat recovery VRF systems market was not an exception. It reduced the manufacturing activities, lowering the water-cooled heat recovery VRF systems requirement. In 2020, there was a 1.4% and 2.2% decline in the manufacturing industries of New Zealand and Australia respectively. Moreover, the pandemic significantly increased the unemployment rates, lowering the disposable income, and consequently reducing the purchasing power of consumers. Resultingly, corporations witnessed huge losses due to declining sales and piling up the inventory. Furthermore, lockdowns were imposed in several economies to curb the spread of the virus. This led to the temporary shutdown of commercial offices and buildings. Additionally, there was a rising inclination toward the work-from-home culture by numerous corporations, which gradually ruptured the requirement for office spaces. Nonetheless, the Australia and New Zealand water-cooled heat recovery VRF systems market is recovering significantly, increasing the office occupancy rates because of the transmission risk aversion and reducing social restrictions. Within the application segment, the healthcare category will exhibit the swiftest growth in the coming years. This can be credited to the growing geriatric population, rising incidence of chronic illnesses, surging disposable income, and enhancing healthcare infrastructure in these countries. Therefore, the robust growth in the market is due to the development of clinics and hospitals to meet the demands of the skyrocketing population levels. A key aspect of medical care is making patients comfortable, which pushes the requirement for appropriate HVAC systems. Hence, the snowballing demand for VRF systems will drive this market.  A number of factors, such as the surging deployment of unified communication systems, increasing investments in corporate telephony, and rising need to improve productivity and reduce operational cost and time, are expected to drive the growth of the corporate telephony market during the foreseeable period (2021–2030). Moreover, the market is witnessing the increasing incorporation of the internet of things (IoT) with communication systems. IoT improves mobility and enables access to data virtually, by allowing data exchange among various divisions over a wireless network. This leads to better work scheduling and improved communication.

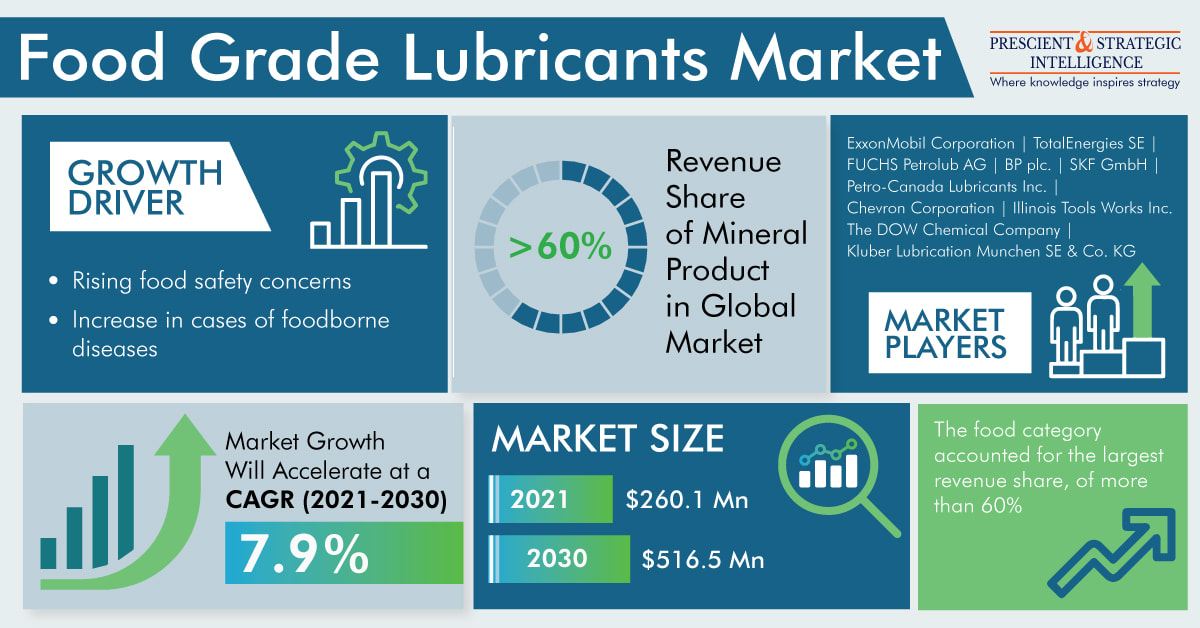

The surging deployment of unified communication systems is one of the main factors boosting the growth of the corporate telephony market. Organizations are rapidly adopting these systems to improve their communications and reduce their operational costs. Moreover, unified communication systems help organizations in improving the user experience, enhancing productivity, and increasing mobility and flexibility. These systems also act as an auto attendant for incoming calls and offer emergency services. Browse detailed report - Corporate Telephony Market Analysis and Demand Forecast Report Furthermore, the increasing investment for the development of corporate telephony is driving the market growth. Many organizations and investors from the private and public sectors are showing interest in corporate telephony to streamline the communication infrastructure efficiently and make coordination easy. Thus, several IT organizations, such as IBM Corporation, Mitel Networks Corp., Cisco Systems Inc., NEC Enterprise Solutions, Interactive Intelligence Group Inc., Huawei Technologies Co. Ltd., and Microsoft Corporation, are investing heavily in this technology. Based on technology, the corporate telephony market is classified into internet protocol-private branch exchange (IP-PBX), wireless private branch exchange, key telephone system, and others. The IP-PBX category is expected to witness significant growth during the forecast period. This can be ascribed to the several advantages offered by the IP-PBX technology, such as lower operating costs, increased agility, high quality of communication, flexible call routing, and robustness and worry-free scalability. These features help organizations in enhancing the productivity of their employees. Moreover, on the basis of industry, the corporate telephony market is categorized into information technology (IT), retail, government, manufacturing, healthcare, banking, financial services, and insurance (BFSI), and others. Among these, the IT category held the largest share in the market in 2020, which is attributed to the escalating developments in telephony technology. Moreover, corporate telephony supports in sustaining a smooth workflow in the IT sector by offering efficient communication. Moreover, it is a simple, cost-effective, and flexible technology. According to P&S Intelligence, the North American corporate telephony market accounted for the largest share in 2020, globally. This was mainly due to the presence of several major industry players, surging adoption of unified communication systems by several organizations, increasing deployment of conference calling and desk-to-desk calling solutions, large number of end users, mounting competition among the players, and rising investments by the IT and BFSI industries in these solutions in the region. Thus, the surging adoption of unified communication systems and the increasing investments in the development of corporate telephony are projected to propel the market growth in the coming years.  The food-grade lubricants are oil and greases used in the agri-food industries or any other industry. These lubricants are validated for incidental food contact, as they are edible and do not pose any threat to health on consumption. A food-grade lubricant might come in accidental contact with the food products being manufactured in the industry, due to leakage, lubrication fault, or overflow.

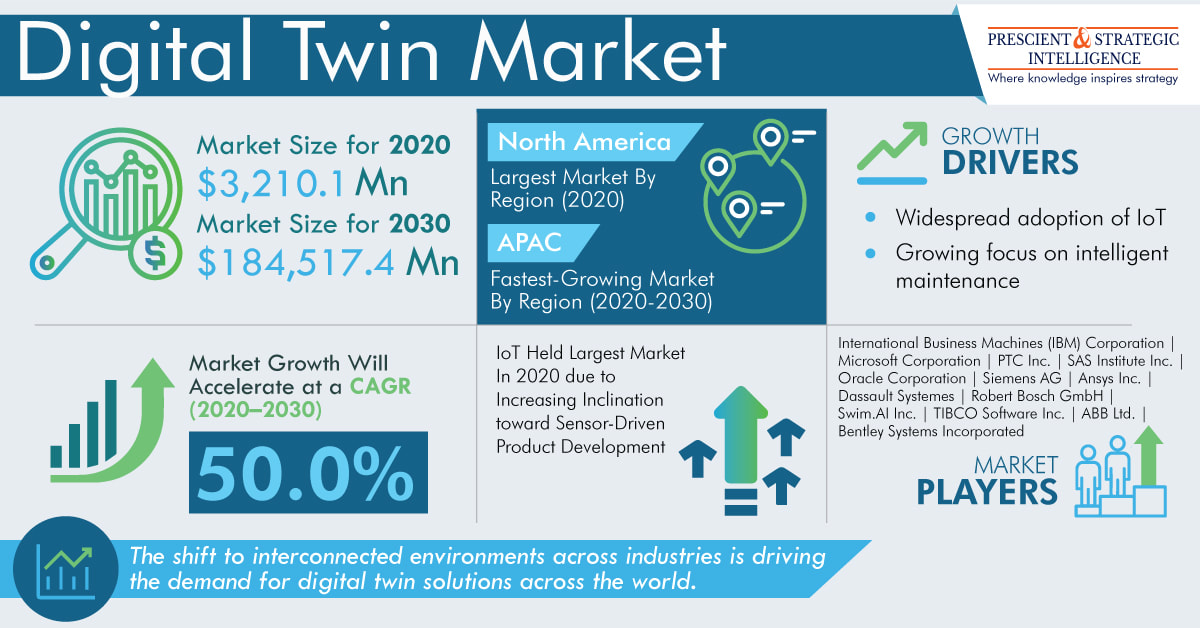

Health and safety priorities for food, drink, and drug manufacturers. It is crucial to maintain cleanliness and hygiene on the shop room floor, as well as in the operating rooms of the hospital. Lubrication poses greater importance in production equipment. As they protect against friction, corrosion, oxidation, heat dissipation, and transfer of power. Lubricants hold compatibility with rubber and other sealing material. They do not behave indifferently against materials with which they come in contact. Therefore, the pharmaceutical and food-processing industries pose additional challenges in selecting the appropriate lubricants for performing the role. Lubricants might be subjected to intense environmental contaminants. The corn-milling industry generates a large amount of dust. Although, it is not as hard as silica-based dust, but results in filtration problems. A meat plant needs effective steam cleaning at all times, to decrease the risk of water contamination. Several plants experience around 15% of water content in their gear oils. Besides this, another major concern is lubrication contamination which poses a greater risk to food-grade lubricants by enabling the growth of the microorganisms such as fungi, yeast, and bacteria. Moreover, these can cause a threat to industrial environments by providing an opportunity to contaminate the food-production environment. In 2021, the food grade lubricants industry generates sales worth $260.1 million, and it is projected to rise at a rate of 7.9% and reach $516.5 million in 2030. It is led by rising safety concerns around the world due to rising incidences of foodborne diseases. Globally, 650 million people around the world are suffering from food-borne diseases. Numerous food-related diseases are caused by the accidental contact of lubricants in the machinery. Therefore, it is highly required for food-grade lubricants for protecting raw materials, as well as finished products from contamination. The transforming lifestyle of people has caused a mass shift in the consumer preference for ready-to-eat packaged food products. It is led by hectic schedules, a shortage of time to cook food, and growing demand for processed food. Therefore, it results in growing sales of processed food products. Therefore, the growing demand for processed food leads to increased consumption of food-grade lubricants. Moreover, the expansion of the food processing industry, and rising food safety concerns led by increasing incidences of food-borne diseases boost the food-lubricants demand.  The surging adoption of advanced technologies, including the internet of things (IoT), machine learning (ML), artificial intelligence (AI), and 5G; rising penetration of Industry 4.0 standards; growing focus on intelligent maintenance; and increasing need for cloud services are expected to drive the growth of the digital twin market at a CAGR of 50.0% during 2020–2030. According to P&S Intelligence, the market size is projected to reach $184,517.4 million by 2030 from $3,210.1 million in 2020. Moreover, the market is witnessing the increasing use of common platforms for digital twins.

The surging adoption of IoT for interconnecting environments across several sectors is one of the main factors boosting the digital twin market growth. For instance, over 41 billion connected IoT devices are likely to be adopted by 2025. For the successful execution and operation of IoT devices, the digital twin technology is essential, being used to improve the performance and lifetime of a system. Additionally, product developers and vendors are increasingly embracing this technology in order to reduce operational costs and speed up the marketing of products. Access Report Summary - Digital Twin Market Segmentation Analysis Report Another major factor behind the growing demand for the digital twin technology among large, small, and medium enterprises is their rising focus on intelligent maintenance. Before the advent of sensors, it was impossible to predict when a machine will malfunction, and when it did, the entire production process would get stalled. Thus, digital twins are now being used to leverage the data being gathered by the sensors embedded in the individual components of a machine to simulate their real-time functioning, so that predictive maintenance becomes possible. Based on application, the digital twin market is classified into product design & development, predictive maintenance, performance monitoring, inventory management, business optimization, and others. Out of these, the predictive maintenance category is expected to witness the fastest growth during the forecast period (2021–2030). This can be ascribed to the surging use of this technology to gather real-time information, estimate downtime, automate operations, and schedule maintenance by creating a digital duplicate of a system, product, or process, in order to achieve operational efficiency. Moreover, on the basis of industry, the digital twin market is categorized into manufacturing, oil & gas, automotive, energy & utilities, healthcare, aerospace & defense, and others. Among these, the manufacturing category held the largest share in the market in 2020. This is attributed to the escalating penetration of Industry 4.0 standards and rising adoption of industrial internet of things (IIoT) platforms across the globe. Moreover, the technology supports manufacturing companies in improving productivity and reducing operational costs by helping in product designing, process optimization, quality management, and preventative maintenance. Globally, the North American digital twin market accounted for the largest share in 2020. This was mainly due to the surging adoption of advanced technologies, such as IoT, ML, AI, and 5G, across the manufacturing, energy, automotive, and aerospace sectors and the development of the IT infrastructure. Whereas, the Asia-Pacific (APAC) is projected to record the fastest growth during the forecast period. This can be attributed to the rising investments in the IT infrastructure, growing regional economy, and increasing adoption of advanced technologies for improving product quality and reducing production time. Thus, the surging adoption of advanced technologies and the increasing penetration of Industry 4.0 standards across the world are projected to propel the market growth in the coming years.  A number of driving factors such as the soaring urban population, escalating construction activities in the commercial and residential sectors, and rising preference for high-end products will propel the North American acid-etched glass market at a 5.5% CAGR during the forecast period (2021–2030). According to P&S Intelligence, the market generated revenue of $237.3 million in 2020, and it is projected to generate $403.1 million by 2030. Additionally, the increasing preference for etched decorative glass doors and windows is also supporting market growth.

Construction activities have spiked in the region, on account of the rapid urbanization. The growing urbanization has been a result of booming population, especially in urban areas. For instance, according to the World Population Prospects 2019, North America is the most urbanized region, with nearly 82% people dwelling in cities and towns. Thus, the rapid urbanization has led to the significant rise in investment for the development of commercial and residential infrastructure, which, in turn, drives the demand foracid-etched glass. Browse detailed - North America Acid-Etched Glass Market Revenue Estimation and Growth Forecast Report Moreover, amplifying demand for etched decorative windows and doors is driving the North American acid-etched glass marketgrowth. Residential and commercial users are adopting large quantity of etched glasses for decorative purposes, due to their magnifying focus on an array of gradients, shades, and textures in glass. These beautifying materials also provide several gradients and opacities to meet the varied needsof the customers. These doors and windows cut down glare, heat, and flame, enhance aesthetic quotient, provide security from external environment, prevent penetration of ultraviolet (UV) radiations,and improve lighting. Furthermore, the expansion of the tourism and hospitality sector in the region will also facilitate the North American acid-etched glass marketgrowth in the foreseeable future. The growth of this industry will lead to the construction of numerous resorts and hotels in the coming years. Hospitality units,such as hotels, resorts, restaurants, and home stays, are expected to adopt a large number of acid-etched glass doors, windows, shelves, railings, and partition walls, to enhance their ambience and attract more customers. The thickness segment of the North American acid-etched glass marketis classified into 4 mm, 5 mm, 6 mm, 8 mm, 10 mm, and 12 mm. Under this segment, the 4 mm category accounted for the largest market share in 2020. This is ascribed to the increasing application of 4mm acid-etched glass in the production of windows, which are widely used in commercial and residential complexes. Moreover, lower cost of 4 mm glass, as compared to other types, also fuels the demand for this type of glass in North America. Geographically, the U.S. generated higher revenue for the North American acid-etched glass market in 2020. This is due to the surging number of government initiatives to amplify tourism and the growing construction industry in the country. The demand for the glass in this nation was met by key players like Bear Glass,OcuGlass LLC,Dillmeier Glass Company,Compagnie de Saint-Gobain S.A., Guardian Industries Holdings LLC,Cosmopolitan Glass INC.,Asahi Kasei Corporation,General Glass International, and CARVART. Thus, the growth of the tourism and hospitality industry and the surge in construction activities in the residential and commercial sectors will boost the market growth in the forecast years. The rapid growth of the manufacturing sector in the last few years has caused a sharp surge in the sales of compressors in India. Moreover, with the implementation of favorable government policies, this trend is likely to continue in the future years. According to industry experts, the manufacturing sector in the country is predicted to attain a valuation of $1 trillion by 2025. In manufacturing facilities, industrial air compressors are heavily used for clamping, stamping, and tool powering.

Apart from the enactment of supportive government policies, the inflow of huge foreign direct investments (FDIs) is also fueling the growth of the country’s manufacturing sector. For example, the government has reduced the income tax rate to 25% for all organizations having a maximum turnover of $38.75 million, under the Union Budget 2018—2019. Besides this, the flourishing automotive industry is also pushing up the sales of compressors in the country. Read More: India Compressor Market Analysis and Demand Forecast Report This is subsequently driving the advancement of the Indian compressor market. The market valuation is predicted to rise from $1,943.4 million to $2,891.9 million from 2019 to 2030. Furthermore, the market is predicted to advance at a CAGR of 6.2% between 2020 and 2030. There are mainly two types of compressors used in India— rotary and positive displacement. Of these, the sales of the positive displacement compressors were found to be higher in the past years. This trend is predicted to continue in the upcoming years as well. This would be a result of the growing requirement for compressors in various industries such as semiconductor, automotive, chemical, and steel. Additionally, the advent of enhanced rotor profiles, innovative designs, improved machines, and various other advanced features is boosting the sales of the positive displacement compressors across the country. When lubrication type is taken into consideration, the Indian compressor market is classified into oil-free and oil-flooded. Of these, the oil-flooded category recorded higher growth in the market in the years gone by, as per the findings of P&S Intelligence, a market research company based in India. This was mainly because of the lower initial cost and lesser maintenance requirements of this lubrication than the oil-free one. Moreover, the price-conscious nature of the Indian consumers and their demand for effective solutions at affordable prices propelled the sales of the oil-flooded lubrication in the past few years. The Indian compressor market recorded considerably high growth in the northern region in the past and this trend will continue in the upcoming years as well. Compressors are extensively used in industrial and automotive manufacturing applications in this region. Furthermore, the usage of the compressors is currently being observed to be very high in the National Capital Region (NCR), primarily because of the rapid industrial growth and soaring automobile manufacturing in this region. Thus, it can be safely concluded that the sales of compressors would skyrocket all over India in the coming years, mainly because of their growing requirement in the manufacturing sector and automotive industry and the explosive growth of the manufacturing sector in the country. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

September 2022

Categories |

RSS Feed

RSS Feed