WORLDWIDEANALYSIS

The burgeoning requirement for real-time data analysis is one of the major factors fueling the demand for data warehouse as a service (DWaaS) solutions across the globe. With increasing digitization, huge volumes of semi-structured, structured, and unstructured data are being generated. Many organizations around the world are leveraging this information for improving their productivity, retaining customers, augmenting their profits, and reducing future risks. Due to this reason, the worldwide demand for big data analyzing and storing solutions is rising rapidly.

The adoption of DWaaS solutions allows the deployment of third-party business intelligence (BI) applications. Besides these factors, the surging adoption of cloud-based solutions is also positively impacting the demand for DWaaS technology all over the globe. Furthermore, the surge in e-commerce sales, on account of the growing internet penetration and the mushrooming usage of smartphones, is creating lucrative growth opportunities for the DWaaS technology developing companies all over the world. Get More Insights: Data Warehouse as a Service Market Revenue Estimation and Growth Forecast Report As per many reports, 3.47 billion people across the world are currently using the internet. This is making companies switch to digital platforms for selling their products and services. Moreover, online platforms provide better deals, easy price comparisons, home deliveries of products, greater product varieties, and 24X7 hassle-free and comfortable shopping experience to customers. Many retailers are increasingly adopting BI tools on data warehousing solutions for providing a personalized experience to customers. Due to the above-mentioned factors, the demand for DWaaS solutions is growing rapidly across the globe. This is, in turn, driving the expansion of the global data warehouse as a service (DWaaS) market. As a result, the valuation of the market is predicted to grow from $1.4 billion in 2019 to $23.8 billion by 2030. Furthermore, the market is predicted to advance at a CAGR of 29.2% between 2020 and 2030. Depending on type, the market is divided into operational data store (ODS) and enterprise data warehouse (EDW) categories. Between these, the ODS category is predicted to exhibit faster growth in the DWaaS market in the forthcoming years. This will be because these solutions enable the integration of data from various sources on a single platform, which, in turn, makes operational reporting easier and hassle-free. Furthermore, ODS utilizes BI tools for deriving useful inferences from the generated data. Across the globe, the DWaaS market will demonstrate the fastest growth in the Asia-Pacific (APAC) region in the upcoming years. This will be because of the growing usage of cloud-based data warehousing solutions by financial institutions, insurance companies, and banks in the region. Moreover, various regional countries such as India, Singapore, Hong Kong, and Australia are witnessing surging digital transformation, which is subsequently pushing up the requirement for DWaaS solutions in the region. Hence, it is safe to say that the demand for DWaaS solutions will skyrocket all over the world in the coming years, primarily because of the growing penetration of the internet, the rising digital transformation, and the burgeoning requirement for real-time data analysis.

0 Comments

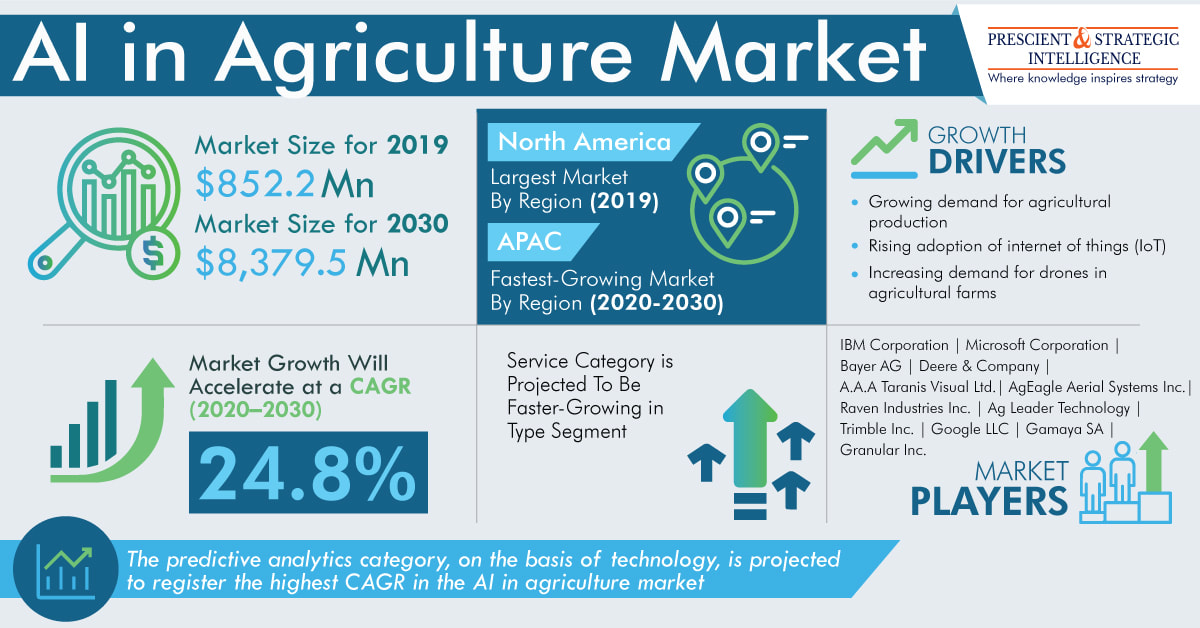

The rising penetration of the internet of things (IoT) technology in the agriculture sector, mounting demand for high crop yields, increasing deployment of drones for pesticide spraying, surging need for real-time livestock monitoring, and growing focus on improved crop management are expected to drive the artificial intelligence (AI) in agriculture market at a CAGR of 24.8% during the forecast period (2020–2030). The market revenue stood at $852.2 million in 2019, and it is projected to reach $8,379.5 million by 2030.

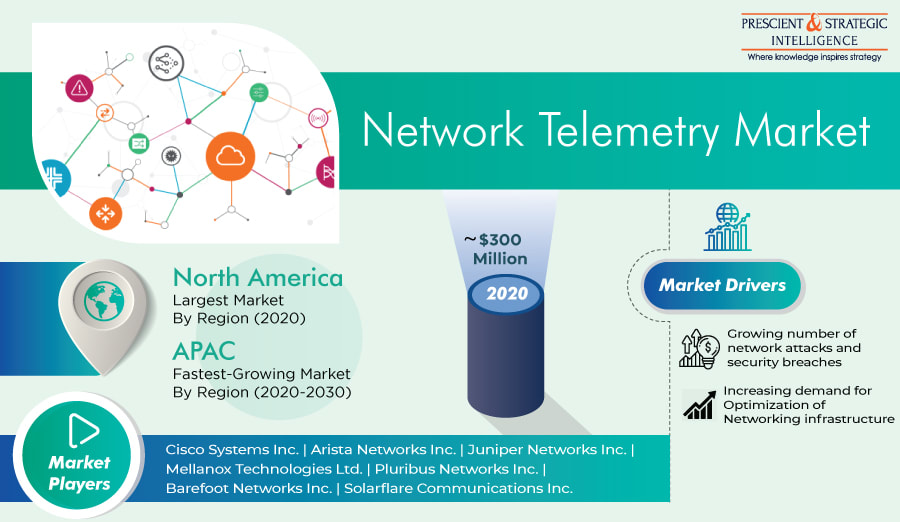

The increasing adoption of drones by farmers has become a key growth driver for the market. Drones are being used for scanning soil health, estimating yield data, applying fertilizers, and assisting in irrigation schedules. Moreover, the surging number of government initiatives facilitating the adoption of drones for improving agricultural practices is having a positive impact on the market. For example, in January 2019, the state government of Maharashtra, India, partnered with the World Economic Forum (WEF) to enhance agricultural yield by gathering details about agricultural farms through drones. Read Full Report: AI in Agriculture Market Revenue Estimation and Growth Forecast Report Moreover, the soaring requirement for real-time livestock monitoring is supporting the AI in agriculture market growth. Dairy farms can easily monitor their herd by using advanced AI solutions, such as image classification integrated with the body condition score and feeding patterns of animals and facial recognition. Farmers are also using machine vision to track the health of their livestock. Machine vision helps in identifying the facial features and hide patterns, recording body temperature and behavior, and monitoring the water and food intake of the rudiments. The categories under the type segment of the AI in agriculture market include product and service. During the forecast period, the service category will grow at the faster pace due to the burgeoning requirement for proper installation, training, and maintenance services among farmers and other industry stakeholders. The category is further divided into professional and managed. Of these, the professional category will witness the faster growth in the coming years owing to the booming demand for maintenance, support, and training services from farmers using AI solutions. Geographically, the North American region recorded the highest demand for such solutions during the historical period (2014–2019), and it is expected to lead the AI in agriculture market in the forecast years as well. This will be due to the early adoption of computer vision and machine learning (ML) technologies for agricultural applications, including soil management, livestock management, greenhouse management, and precision farming. Moreover, the surging integration of IoT with computer vision will support the market growth over the forecast period. The Asia-Pacific (APAC) AI in agriculture market is projected to record the fastest growth in the forecast years. This can be primarily owed to the high adoption rate of AI solutions in the agriculture industry in Australia, India, China, and Japan. Among APAC nations, China is witnessing a widespread adoption of the AI technology in agriculture due to the entry of Alibaba Group in the agricultural solutions business with its AI technology to aid the small farmers in the nation. Thus, the rising utilization of drones on farms and increasing need to monitor the livestock on a real-time basis will propel the market growth in the coming years.  The world is currently witnessing a significant surge in the number of cyberattacks, due to the increasing penetration of the internet. The servers and networks of business organizations and government agencies are constantly under the threat of network attacks and security breaches, which lead to enormous data and financial losses. Hackers are stealing data from multiple sources in the workplace, such as the internet of things (IoT) gadgets, that are linked to a centralized network. To avoid such cybercrimes, organizations across the world are opting for network telemetry services and solutions.

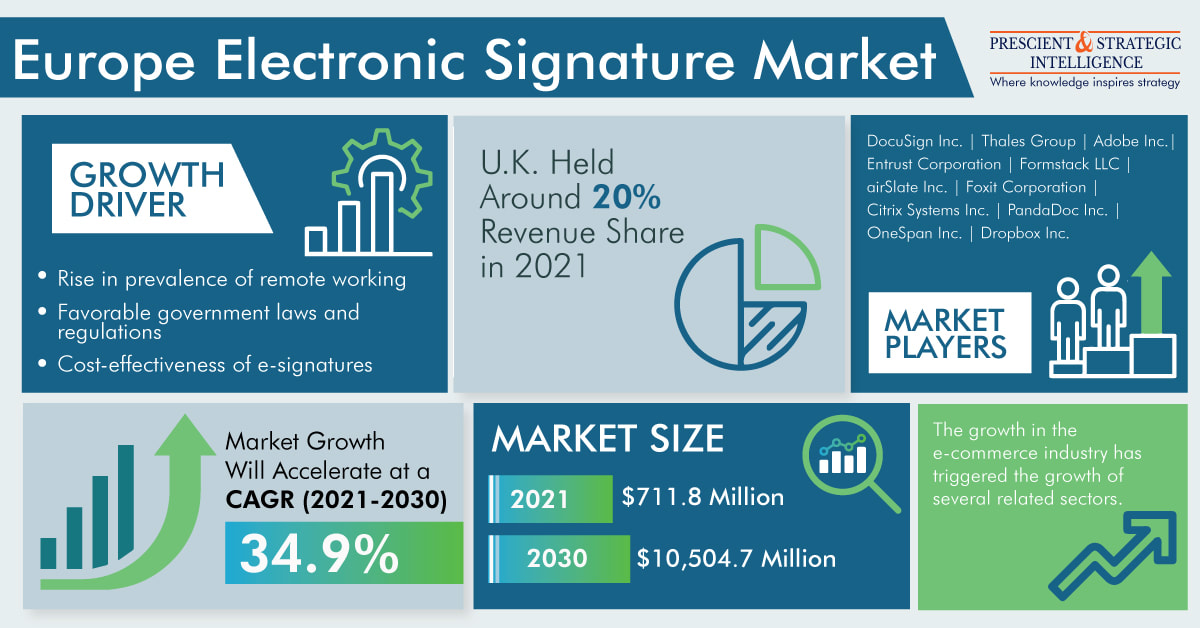

Moreover, the burgeoning need for optimization of network infrastructure, owing to the rapid digitization, will also support the network telemetry market growth during 2021–2030. According to P&S Intelligence, the market was valued at $200 million in 2020. Rapid digitization has resulted in a rise in internet traffic, which is often characterized by downtime issues. For example, when real-time data is transmitted to more than one location through network devices, the system becomes unavailable for a short duration, thereby, resulting in downtime. This issue can be solved by the deployment of network telemetry solutions. Get More Insights: Network Telemetry Market Revenue Estimation and Growth Forecast Report Additionally, the continuous developments in technologies such as IoT and artificial intelligence (AI) will also create a huge requirement for network telemetry solutions and network telemetry professional and managed services in the coming years. The increasing adoption of such advanced technologies in large enterprises and small and medium-sized enterprises (SMEs) will result in the large-scale deployment of network telemetry solutions in such enterprises in the foreseeable future. Organizations of various sizes are adopting cloud-enabled and on-premise solutions to enhance their data security and manage their network communication infrastructure. At present, network telemetry services and solutions provided by Cisco Systems Inc., Solarflare Communications Inc., Arista Networks Inc., Marvell Semiconductor Inc., Pluribus Networks Inc., Barefoot Networks Inc., Juniper Networks Inc., VOLANSYS Technologies Pvt. Ltd., Mellanox Technologies Ltd., and Netronome Systems Inc. are being used by telecom service providers, managed service providers, and cloud service providers. Currently, the solutions and services offered by these companies are majorly used by telecom service providers to analyze, manage, and optimize their network communication infrastructure. In recent years, network telemetry solution providers have been forming partnerships to expand their clientele. For instance, in May 2019, Pluribus Networks Inc. partnered with Vapor IO Inc. to position its Adaptive Cloud Fabric and Netvisor ONE operating system (OS) 5.0 at many kinetic edge sites of Vapor IO Inc. in the US. Under this partnership, Vapor IO Inc. is using comprehensive telemetry capabilities to connect its data centers. Likewise, in October 2019, Juniper Networks Inc. and Telefonica UK Limited came together to build a cloud-enabled secured and automated network infrastructure named Fusion Network. Geographically, North America dominated the network telemetry market in the recent past, and it would demonstrate notable growth in the forthcoming years. This can be primarily credited to the presence of a large number of network telemetry solutions providing companies, such as Netronome Systems Inc., and Cisco Systems Inc., Arista Networks Inc., and Cisco Systems Inc., in the region. Additionally, the early adoption of technologies such as IoT and AI also amplifies the need for network telemetry services and solutions in the region. Therefore, the rising data breach incidents and escalating need to optimize network infrastructure will augment the adoption of network telemetry solutions in the forthcoming years.  Since the outbreak of COVID-19, a great shift has been witnessed in the global work culture. Owing to the existence of advanced technologies and high-speed internet, economies could deal with the disruption in the functioning of numerous industries, with the mass adoption of remote work policies. Due to this factor, the revenue generated by the European e-signature market was $711.8 million in 2021. It will advance at a massive CAGR of 34.9% from 2021 to 2030 and reach $10,504.7 million by the year 2030.

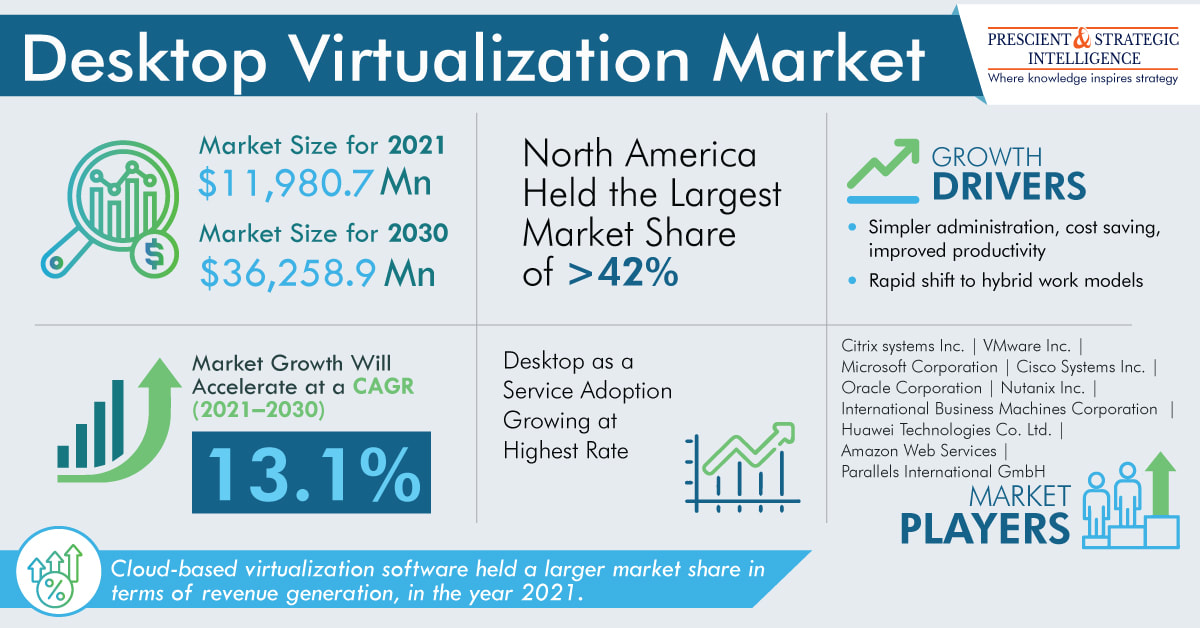

It is believed by European business leaders that organizations that have shifted to hybrid work models are more profitable. Indeed, remote working and hybrid work models are the major drivers of the European e-signature market. The rising in the volume of online documentation processes, cost-effectiveness of e-signatures, and favorable government laws have played a great role in the growing trend of remote working even after the lifting of COVID-19 lockdowns. The increased efficiency, cost savings, timeliness, instant support, and many other benefits have made it feasible to shift to hybrid work models for the long term. Browse detailed report - Europe Electronic Signature Market Analysis and Demand Forecast Report The fact that one does not need to move from one place to other, thus saving the travel expenditure and time, is the major factor behind the mass adoption of e-signatures. Almost every sector, such as BFSI, corporate communications, legal, and marketing, is utilizing this technology to carry out business processes. A one-time digitized scanned signature can be utilized several times for multiple purposes. Digitization has led to the growing demand for e-signature solutions for various purposes, such as opening a bank account and filing income tax returns. Considering the security concerns, electronic signatures protect individuals’ identitities and help manage regulatory compliance. They also provide assistance to BFSI personnel in simplifying the complex business processes with enhanced security and a faster onboarding of customers. Therefore, the BFSI category generated 40% of the European e-signature market revenue in 2021, under the vertical segment. Government institutions have also adopted digital transformation of the work processes by utilizing e-signature software. Human resource (HR) departments also capitalized on the opportunity, by adapting to digital onboarding processes, to keep themselves functional during COVID-19 lockdowns. The constantly growing e-commerce sector is creating more opportunities in the European e-signature market. Businesses are shifting their processes online, and e-signatures are required to legally bind documents, to govern and facilitate the accommodation of such transition. Security, being the major concern here for sensitive documents, needs a significant solution. The rise in the internet penetration has also resulted in a significant increase in the cyber-crime prevalence, such as theft of information and money and online fraud. Since online transactions have made merchant processes easier, their volume is significantly increasing. In the European e-signature market, the U.K. held a 20% revenue share in 2021, the largest in the continent. It is because e-signatures are widely being utilized for online identification in the country, as they are crucial for services facilitated by the World Wide Web. In order to identify the individual through his or her documents, such as passport, photo ID card, and driving license, there is a specific platform. It has made it easier for the residents of the U.K. to access government services, such as filing for tax or tracking application status. Hence, the increased efficiency and cost-effectiveness provided e-signatures are the major driving factors behind the boom in the market.  Client/server architecture is the standard foundation for desktop virtualization, in which the organization's preferred operating system and applications operate on a server housed either in a data center or in the cloud. This architecture is reminiscent of the so-called "dumb" terminals that were common on mainframes and early Unix systems, where all user interactions take place on a local device of the user's choosing.

Moreover, in comparison to traditional desktop computers, it has several benefits, including easier administration, lower costs, more productivity, support for a wide range of kinds of devices, agility and scalability, stronger security, and better operator experiences. The desktop virtualization market is on the track to hit $36,258.9 million by 2030, growing at a 13.1% CAGR from 2021 to 2030. Browse detailed report - Desktop Virtualization Market Analysis and Demand Forecast Report The cloud-based category held a larger market share in terms of revenue generation, in the year 2021. Through the internet, cloud-based computing provides access to software that is using shared resources including processing power, disc storage, and memory. These computer resources are maintained by remote data centers, which were designed specifically to host programs on various platforms. North America holds the largest share in the global desktop virtualization market. This is mostly credited to the region's advanced IT infrastructure, which was made possible by significant IT investment, adoption of 5G technology, and early adoption of cloud-based technologies. This technology is widely used at universities, colleges, and K–12 district schools, which explains why there is a high requirement for virtual desktop software in this area than elsewhere. Types of Desktop Virtualization In the desktop virtualization market, the three most common types of desktop virtualization: Remote desktop services (RDS), Desktop-as-a-Service (DaaS), and Virtual desktop infrastructure (VDI). • By giving service providers the role and responsibility for desktop virtualization, DaaS significantly decreases the strain on the IT department. The predictable monthly prices that DaaS providers build their business model on will be appreciated by organizations that desire to convert IT spending from capital expenses to operational expenses. The growing need for secure virtual desktops when working remotely, especially now that the epidemic has prompted companies to adopt hybrid work practices. This is why, DaaS generated about 25.0% of the desktop virtualization market revenue in past, and it will grow CAGR of 13.5% during the forecast period. • VDI replicates the well-known desktop computing concept and operates on VMs in either an on-premises data center or the cloud. Adopting this strategy allows businesses to administer the desktop virtualization server just like any other on-premises application server. • RDS is frequently used in place of a full Windows or Linux desktop when only a small number of applications need to be virtualized. Applications are broadcast to the local device, which has its own OS, in this manner. Because only applications are virtualized, RDS systems may provide a greater user density per VM. Several big companies in the desktop virtualization software market are continuously busy with innovations of products and enhancing their customer base and position. These companies are Parallels International GmbH, Amazon Web Services, Citrix systems Inc., Microsoft Corporation, Nutanix Inc., Huawei Technologies Co. Ltd., Cisco Systems Inc., Oracle Corporation, International Business Machines Corporation, and VMware Inc.  The rising number of digital transactions in most of the countries in the Americas is one of the biggest factors responsible for the surge in the usage for self-checkout systems in the region. Most of the countries in the region are rapidly shifting toward cashless transactions and economy. For instance, 90% of the population in Canada owned credit cards in 2018. Moreover, the country observed a growth of 7% and 9% in the usage of debit cards and in the total value of the transactions made through debit cards, respectively, from 2016 to 2017.

The other major factor propelling the demand for self-checkout systems in North and South America is the rising shortage of labor in the region. Since the last few years, there has been a massive rise in labor shortage in most of the countries in the region. For instance, the companies in the U.S. are increasingly finding it difficult to find skilled employees, with almost 6.3 million jobs remaining unfilled in the country in January 2018. Moreover, the companies recorded a rise of around 16% in unfilled jobs from 2017 to 2018. Due to the above-mentioned factors, the revenue generated from the sales of self-checkout systems in the Americas is expected to increase from $3.9 billion in 2018 to $7.1 billion by 2024. The Americas self-checkout systems market is predicted to advance at a CAGR of 10.9% during the forecast period (2019–2024). Many companies in the Americas are rapidly adopting the self-checkout systems hardware, software, and services. Out of these, the self-checkout systems hardware observed the highest adoption in the region in 2018, as they transactions cannot proceed without enabling terminals, card readers, and machines. The biggest trend presently being witnessed in the Americas self-checkout systems market is the adoption of mobile scan and go systems across the region. These systems enable the users to use their smartphones for scanning the items that they want to buy from the shop at the service point-of-sale (POS) terminal. The mobile scan and go systems allow the customers to digitally make payments without being in direct contact with any machine, thereby reducing the overall buying time. In the Americas, Mexico is predicted to observe the fastest growth in the adoption of self-checkout systems during the forecast period. This is mainly attributed to the rising adoption of these systems by the major retailers in the country such as Wal-Mart de México, S.A.B. de C.V. In addition to this, the ballooning number of retail stores in the country will further push the demand for self-checkout systems in order to reduce the billing and purchasing time and enhance the shopping experience. Hence, the usage of self-checkout systems in the Americas is certain to surge in the coming years, on account of the increasing popularity of digital transactions and the rapid technological advancements in the region. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

September 2022

Categories |

RSS Feed

RSS Feed