WORLDWIDEANALYSIS

|

The Middle East and Africa (MEA) is one of the hottest regions on earth, with a large part of it covered by two great deserts: the Sahara and Arabian. This is why air conditioners are an important requirement here, especially during the scorching summers. Moreover, with climate change, higher temperatures are being recorded in the region every year. For instance, in 2017, temperatures of around 54 degree Celsius were recorded in Iran, Kuwait, and Iraq. Further, the Max Planck Institute for Chemistry says that the temperature rise in the region will be two-times faster than the global average.

This is why P&S Intelligence expects the Middle East and Africa heating, ventilation, and air conditioning (HVAC) market to reach $10.1 billion by 2024 from $7.8 billion in 2018, at a 4.9% CAGR during the forecast period (2019–2024). Similarly, countries near or on the equator have average humidity of 50%, which makes ventilation systems necessary here. Thus, with the strengthening of the economy of Kenya, Republic of Congo, Uganda, Gabon, and Nigeria, the sale of HVAC equipment is increasing in the MEA region. Browse detailed report - Middle East and Africa HVAC Market Analysis and Demand Forecast Report The economic prosperity in the region is visible in the constant rise in the construction activities here. Many of the construction projects are part of the preparations for upcoming events, such as Dubai Expo 2020 (now rescheduled for 2021) and the FIFA World Cup 2022 in Qatar. In 2018, 106 4-, 5-, and 7-star hotels with a total of 13,733 guestrooms, along with eight football stadia, were under construction in Qatar. Similarly, in a bid to reduce their dependence on oil exports, numerous Gulf Cooperation Council (GCC) countries are giving a boost to other sectors. Once these construction projects are commissioned, a large number of HVAC systems are installed. Among heating, ventilation, and cooling systems, which are the three categories of the HVAC type segment, the cooling category held the largest share in the Middle East and Africa HVAC market in 2018. The cooling category is subdivided into ducted split/packaged units, variable refrigerant flow (VRF), chillers, split units, and room air conditioners (RACs). Among these, ducted split/packaged units dominated the market during 2014–2018 (historical period). This is attributed to the rising number of skyscrapers and data centers in the region, where ducted split/packaged units offer a cost-effective and efficient cooling solution. In the years to come, the installations of VRF units are predicted to increase at the highest pace, especially at hypermarkets/supermarkets, commercial offices, and stadiums, because of their cost-effectiveness. Moreover, due to the growing need to conserve electricity and reduce the rate of environmental degradation owing to carbon emissions, green buildings are being constructed in the region, which is driving the demand for VRF systems. The end user segment of the Middle East and Africa HVAC market is classified into residential, commercial, and industrial, among which the commercial classification generated the highest revenue in 2018. This is attributed to the growth in the region’s hospitality industry and number of commercial buildings. The construction of commercial spaces is being boosted by the government initiatives to diversify their economies. For instance, in Saudi Arabia, the $26.6 billion expansion of Mecca’s grand mosque and construction of the $16.5 billion Haramein high-speed railway are underway. Because of such infrastructure development activities, the highest HVAC sales in the MEA region are registered in Saudi Arabia. Since the recovery in oil prices after the slump of 2014–2015, the Saudi economy has rebounded. This is now driving infrastructure development in the country, such as the Riyadh and Jeddah metro networks. Additionally, the number of pilgrims coming to Mecca and Medina is rising, which is leading the government to give the hospitality sector here a boost, thereby resulting in the increasing HVAC sales in the kingdom. Hence, with more commercial, residential, and industrial units being constructed in a region that is plagued by high temperatures and humidity, the demand for HVAC equipment will increase here.

0 Comments

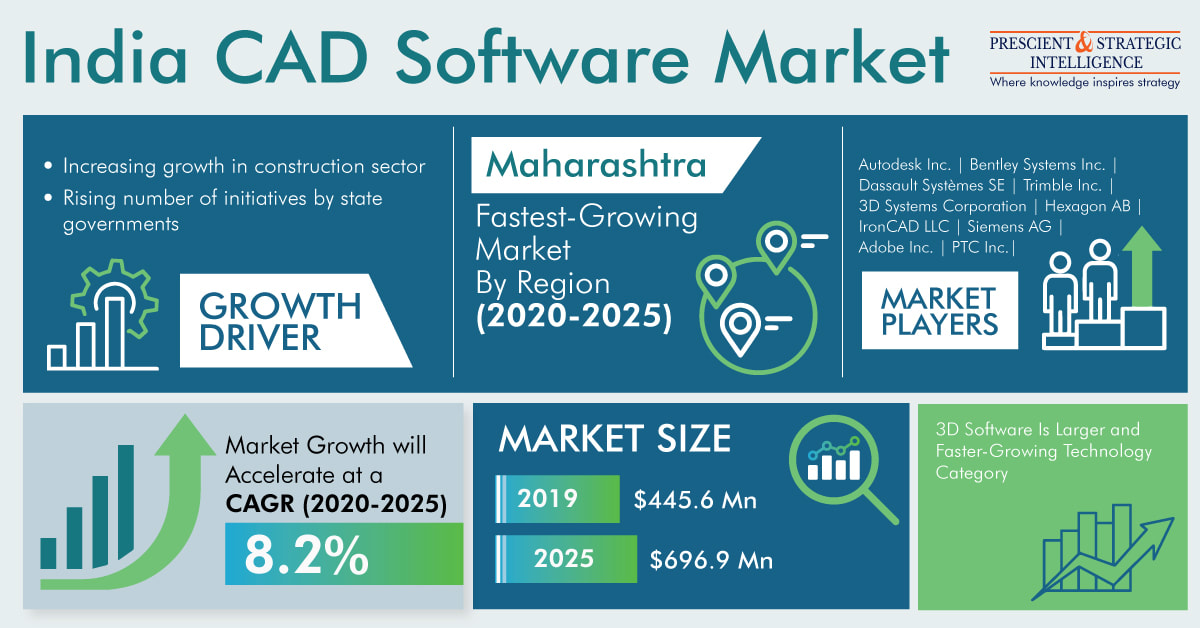

The global computer-aided design (CAD) software market attained a valuation of $9.3 billion in 2019 and it is predicted to advance at a CAGR of 6.6% between 2020 and 2030. According to the forecast of P&S Intelligence, a market research company based in India, the market will generate a revenue of $18.7 billion by 2030. The growing adoption of the CAD software in automotive and manufacturing industries is one of the major factors driving the progress of the market.

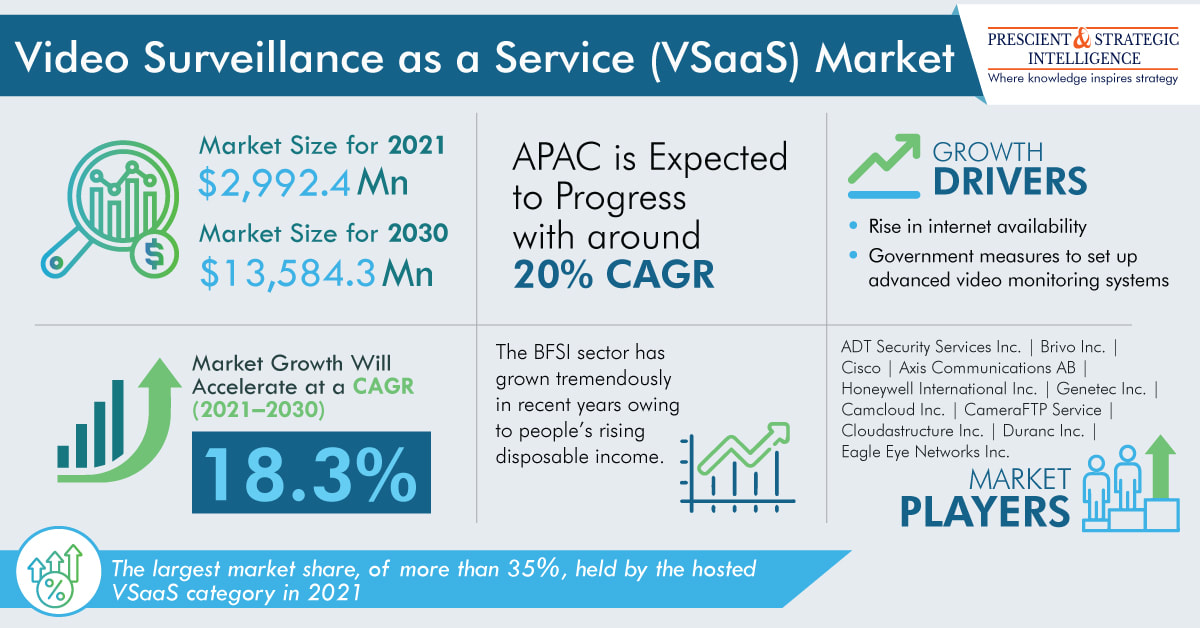

The automotive industry has witnessed a massive rise in the demand for high-quality products and components over the last few years. This factor when coupled with the growing focus of automotive manufacturers on reducing the occurrence rate of product recalls is causing a sharp surge in the demand for the integration of CAD software in automobile manufacturing processes. Moreover, many automakers are increasingly incorporating CAD supported-advanced tools and solutions for facilitating the development and design of connected car components. Apart from the above-mentioned factor, the burgeoning usage of the CAD software in the packaging industry is also fueling the expansion of the CAD software market across the globe. Packaging processes involve the designing, planning, boxing, wrapping, or bottling of products for various end users such as individual customers and military, industrial, and manufacturing industries. These operations along with the associated product filling, strapping, labeling, and wrapping processes are completed with the help of packaging machinery. Browse detailed - CAD Software Market Revenue Estimation and Growth Forecast Report As these machines are becoming more and more complex, designers and engineers are rapidly adopting the CAD software for meeting the mechatronic engineering challenges. The adoption of this software allows the unconventional modeling of these packaging equipment via communication and simulation control tools. Additionally, the mushrooming demand for smart packaging is further boosting the requirement for CAD software around the world, which is, in turn, propelling the expansion of the market. Depending on technology, the CAD software market is divided into 3D software and 2D software categories. Of these, the 3D CAD software category will exhibit faster growth in the market in the coming years. This will be because of the various advantages of the 3D CAD software over the 2D one such as its ability to provide improved product presentation and visualization and the rising requirement for greater accuracy and precision in product drawings all over the world. Furthermore, and the surging adoption of the 3D technology in several application areas is fueling the advancement of this category in the market. Across the globe, the CAD software market will demonstrate the fastest growth in the Asia-Pacific (APAC) region in the forthcoming years. This is credited to the burgeoning adoption of this software in various regional countries such as India, China, and Japan, primarily for several healthcare and automotive applications. Hence, it can be said with full surety that the market will exhibit huge expansion all over the world in the coming years, mainly because of the increasing usage of the CAD software in the automotive and packaging industries.  By 2030, the global video surveillance as a service market is predicted to touch $13,584.3 million, since being valued at $2,992.4 million in 2021. The market will grow at an 18.3% CAGR from 2021 to 2030 owing to the rising number of smart cameras and several accompanying sensors, which has resulted in an inclination toward in-band analytics. This combination of variables will augment growth in the market. For instance, there is extensive use of in-band analytics, smart cameras, and other techniques to facilitate operations.

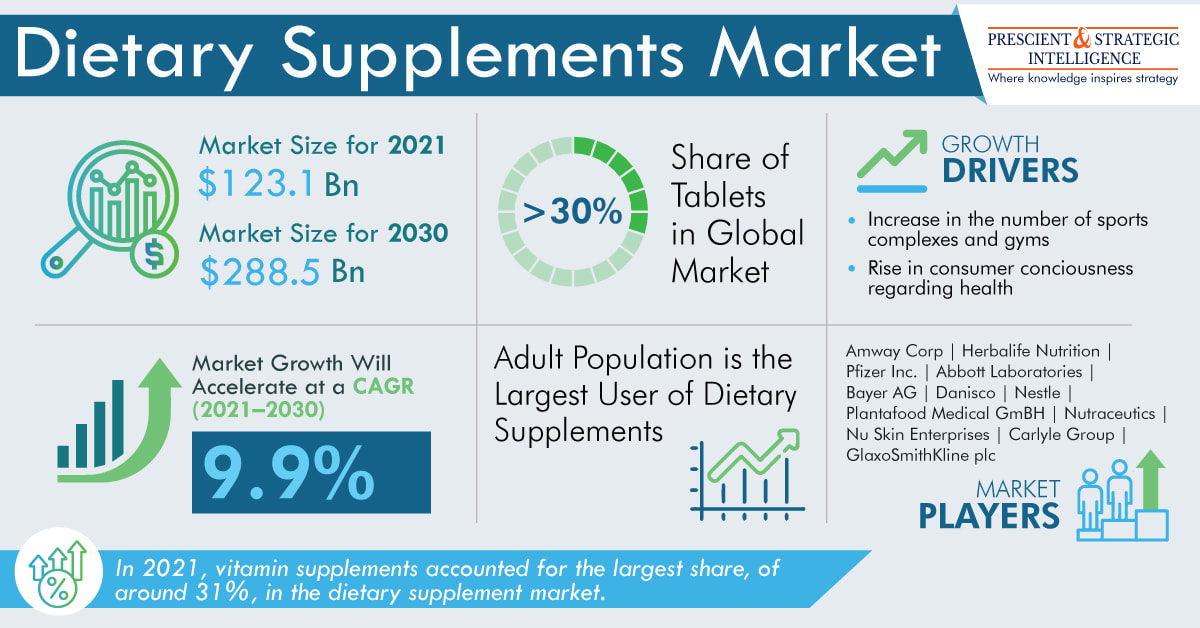

The enormous adoption of cloud-based services is creating lucrative opportunities for the video surveillance as a service market. The swift adoption of technology will help the market players to adapt to the shifts in the tastes and preferences of the consumers and the existing market dynamics. Thus, the rising availability of higher frequency bandwidths and various innovations made in cloud computing technology will drive the global market. Users in the surveillance industry are robustly using cloud-based services to cater to their requirements. There is an inherent benefit of swifter response, evidence tampering prevention, and enhanced reach. Get More Insights: VSaaS Market Revenue Estimation and Growth Forecast Report The surging internet penetration will spur the video surveillance as a service market growth. A market share of at least 35% is held by the hosted category, based on type. This can be ascribed to the extensive utilization of hosted video surveillance as a service in the development of smart cities, and the retail and residential sectors. Moreover, swift-paced internet connectivity, profit-orientation of 5G services, and the surging mobile phone penetration will propel growth in this industry. The lower subscription fees will account for higher sales. Within the vertical segment, the BFSI sector will generate high revenue in the video surveillance as a service market on account of the rising disposable income of the people. The VSaaS provides several benefits including surveillance data access, adding devices flexibility, and lower initial costs. Because of this, these devices are being highly integrated into financial institutions to keep an eye on staff and customers. Furthermore, it also reduces the threats of robberies and kidnapping, enabling the detection of frauds at cash centers to deploy security within banking processes. North America rules the video surveillance as a service market, accounting for approximately 40% of the total revenue. This can be credited to extensive government support, rising threats of terrorism, and surging crime rates in the region. The most usual users of VSaaS are office spaces, restaurants, and hotels. There is an increasing installation of modern surveillance systems by the government in public spaces. In addition, it is also working to expand the usage of these services in the infrastructure and defense industries.  The major drivers in the global dietary supplements market are paradigm shifts in consumer preferences, increasing prevalence of long-term disorders, rising consumer inclination toward physical well-being and health, and snowballing demand for sports nutritional supplements. In 2021, the market stood at $123.1 billion, and it is predicted to touch $288.5 billion by 2030. The market will witness an approximately 10% CAGR from 2021 to 2030. The growth in the market will go hand in hand with the surging consumer awareness toward a healthy lifestyle, and the rising count of gyms and sports complexes.

Within the distribution channel segment, the development of the online retail category will augment growth in the dietary supplements market. There is a surging investment in the R&D activities to adapt to the shifting consumer tastes and preferences to cater to a wide range of consumers. Also, the increasing number of smartphones and rising internet penetration have boosted the sales of this category. Moreover, a surging inclination toward online retail will lead to an expansion of the scope of these products. Moreover, tailoring supplements for a specific consumer bracket will drive the market. Get More Insights: Dietary Supplements Market Segmentation Analysis Report The vitamin supplements category ruled the dietary supplements market in 2021, by accounting for approximately one-third of the total market revenue. The major factor behind this is the rising incidence of vitamin deficiency, including Vitamins E, C, B, and A, among the growing population. Therefore, there is an escalation in the sales of vitamin supplements to meet the daily requirement of vitamins in the people. Moreover, because of the increasing environmental issues, there is a surging integration of the vegan diet, which in turn, propels botanical supplement category growth. The third-highest-used product in the dietary supplements market is the botanical supplement. This can be attributed to its inherent benefits in comparison to synthetic drugs, including greater affordability and better safety with no side effects. There is a paradigm shift in consumer preferences toward botanical products. Furthermore, the lack of a balanced diet among the people exerts a push on their dependency on these products. Moreover, the vitamin supplements are different for people belonging to different age groups, meeting their specifications. The surging inclination toward leading a healthy lifestyle among the aging population will provide lucrative opportunities to the dietary supplements market players including Nestle, Carlyle Group, Nutraceutics, and Nu Skin Enterprises. Essentially, aging drastically shapes the individuals’ societal, physiological, and psychological changes, which in turn, have a major role in their nutritional choices. Moreover, there is a significant shift in the nutritional consumption pattern of adults, making them dependent on these supplements to enhance their overall health conditions. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

September 2022

Categories |

RSS Feed

RSS Feed